Keeping up with credit feels easier when I can see my Equifax credit score and Equifax credit report in one place. I don’t want guesswork, and I don’t want to pay before I know what’s included.

That matters because many people first want to check credit score free USA options before signing up for anything paid. MyEquifax gives me a simple starting point, so I can track changes, improve weak spots, and guard against fraud.

What I can get for free with my Equifax ?

For me, the biggest draw is simple: U.S. users can create a free myEquifax account and view an Equifax credit score and Equifax credit report online. Access is available weekly, no credit card is required, and I can also check updates in the mobile app when I’m away from my desk.

Free score and report access that helps me spot changes fast

Regular access helps me catch small problems before they turn into expensive ones. If a payment shows late, a card balance jumps, or a hard inquiry appears, I can see it sooner and act faster.

That is why free access matters. When I want to check credit score free USA, I don’t only want a number. I want enough detail to spot account errors, watch trends, and see whether my habits are helping or hurting.

When free tools are enough, and when paid monitoring may help

Free myEquifax works well when I mainly want Equifax-based tracking, report access, disputes, and basic fraud tools. For many people, that’s enough for everyday credit care.

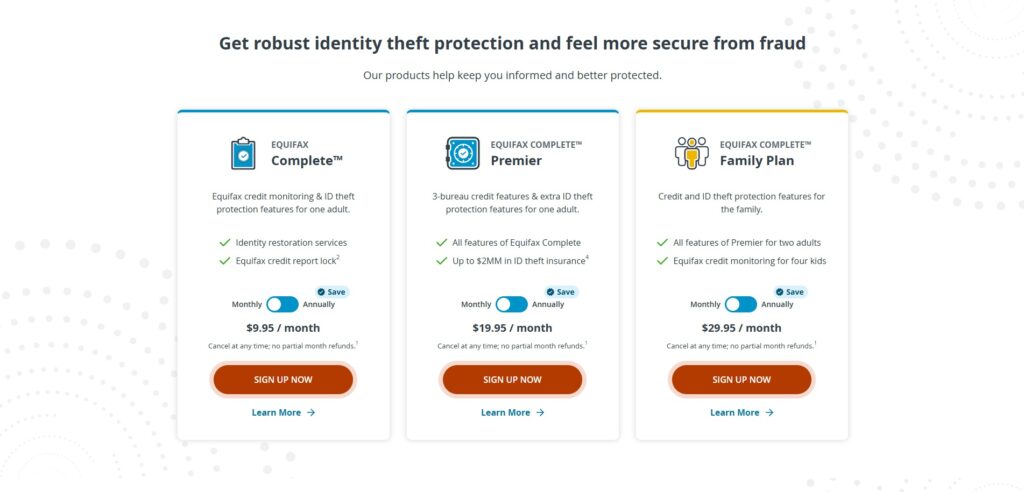

Paid credit monitoring services USA can make more sense if I want three-bureau monitoring, identity theft insurance, and dark web scans. I see those as extras, not must-haves for everyone. If my risk feels low, free tools may cover the basics well.

How I use Equifax tools to improve my credit score over time

I try to focus on the few moves that matter most, because credit improvement isn’t magic. It’s more like tending a garden, small work done often.

I focus on payment history and credit use first

First, I protect my payment history. On-time payments carry the most weight, so I watch due dates closely. Even one missed payment can leave a mark.

Next, I keep card balances low. A common guide is staying under 30 percent of the limit, though lower is usually better. When my dashboard shows balances rising, I know it’s time to pay them down before they drag on my score.

How I use Equifax tools to improve my credit score over time

I try to focus on the few moves that matter most, because credit improvement isn’t magic. It’s more like tending a garden, small work done often.

I focus on payment history and credit use first

First, I protect my payment history. On-time payments carry the most weight, so I watch due dates closely. Even one missed payment can leave a mark.

Next, I keep card balances low. A common guide is staying under 30 percent of the limit, though lower is usually better. When my dashboard shows balances rising, I know it’s time to pay them down before they drag on my score.

A credit lock or freeze can stop new fraud in its tracks

Equifax offers a no-cost security freeze, and lock options are available too. If I spot suspicious activity or hear about a data breach, freezing my file can help block new credit applications in my name.

Fraud alerts and account monitoring give me early warning

Fraud alerts add another layer. They tell lenders to verify my identity before opening new credit, which buys me time if something looks off.

I also like alerts for new inquiries, accounts, or major report changes. That early warning gives me peace of mind and helps me decide whether paid credit monitoring services USA are worth the extra cost.

I don’t need to guess about my credit when I can track my Equifax credit score, review my Equifax credit report, fix errors, and use protection tools as one routine.

If I were starting today, I’d check the free tools first and build from there.